Table of Contents

Categories

Most Popular

Blockchain technology is taking on an increasingly important role in the global economy — and the ecommerce sector is taking notice.

Over 22,000 venues around the world currently allow customers to pay with cryptocurrency,* among them major brands like Expedia, Overstock, and Microsoft. And blockchain in online shopping is only going to gain more traction over the next few years.

But cryptocurrency isn’t the only opportunity that blockchain presents forward-thinking retailers. The benefits of blockchain in ecommerce extend from faster, cheaper business processes to greater data security and an improved customer experience.

Diving into a topic like blockchain technology and blockchain ecommerce marketplaces can get confusing, fast. We’ve distilled the essentials of what blockchain is and why retailers should pay close attention to this important emerging tech.

What is Blockchain?

Blockchain has been a buzzword for a while now, but there’s still plenty of confusion on what it is exactly. Although it’s closely associated with Bitcoin, blockchain is not a type of cryptocurrency. It’s not a programming language. It’s a new technology.

The blockchain is essentially a completely secure online ledger that keeps a record of every transaction made at a given place.

Blockchain technology enables users to share and securely store digital assets. It has applications for payment processing, product searches, and even customer service.

How do blockchains work?

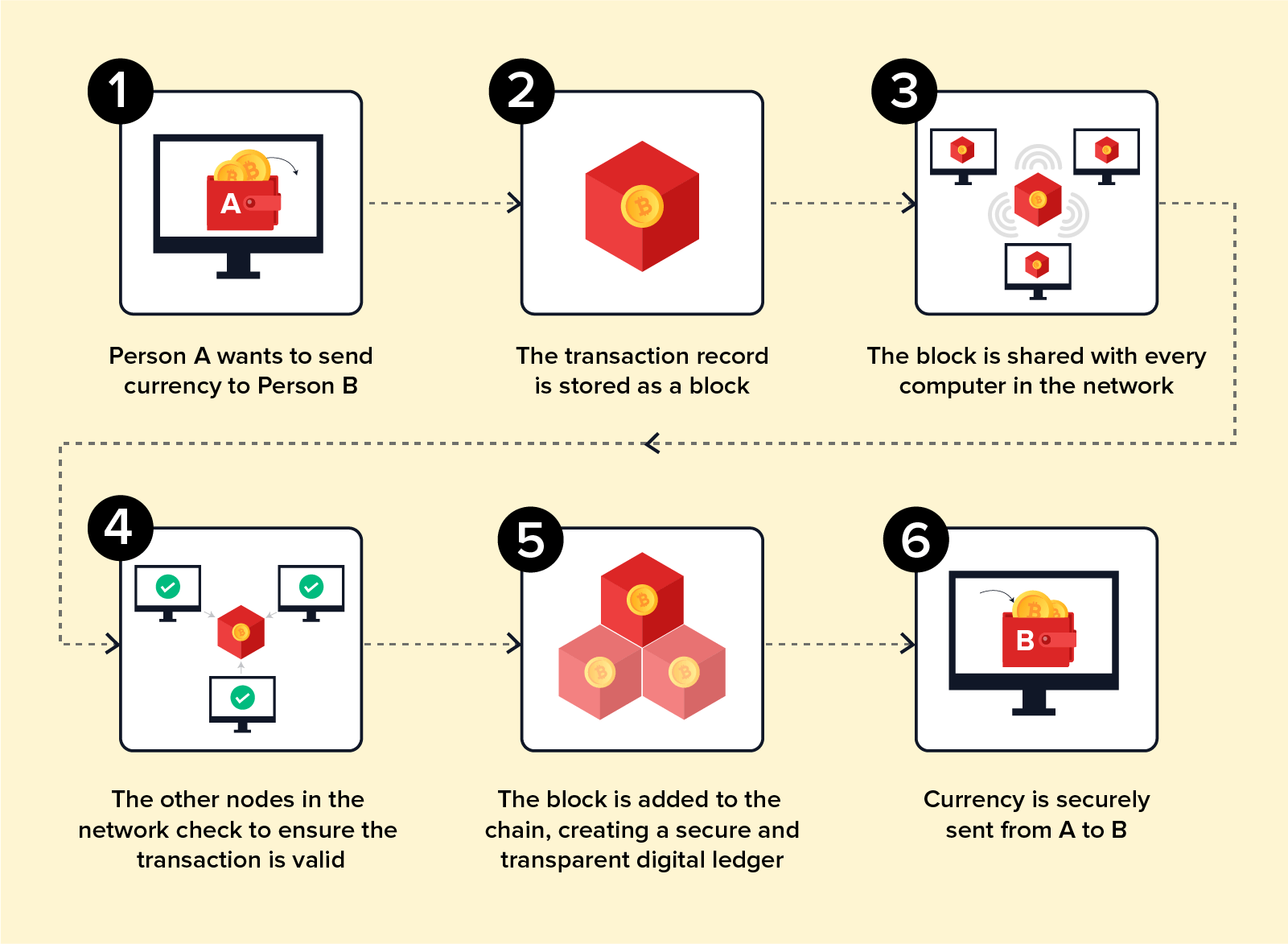

The name “blockchain” comes from the structure of this digital ledger: individual records, called blocks, are linked together in a list, called a chain.

This chain of blocks becomes a database that is shared across a network of computers, also referred to as nodes, miners, or peers. These nodes maintain their blockchain by validating and transmitting data about digital transactions, like the movement of cryptocurrency from one network user to another.

Here’s an example: say you buy a pizza from your friend George and you pay him in Bitcoin. When you send George a Bitcoin, you create and publish an entry in the Bitcoin blockchain. The other computers in the network will check to make sure you haven’t already sent the data representing that bitcoin to another user (preventing you from spending digital currency you’ve already spent). Every computer in the Bitcoin network keeps a record of all the transactions made within the network, and tracks the balance of every account.

Because this ledger isn’t controlled by just one computer and doesn’t have a single point of failure, all entries can be viewed by the entire network. This means data that’s entered in a blockchain can’t be deleted, altered, or corrupted.

Blockchain-based Ecommerce

Because blockchain makes transactions safer and faster, the potential impact on ecommerce is tremendous.

What is the purpose of blockchain applications in business and commerce? The most common blockchain technologies used in ecommerce are Ethereum, which provides a platform for ecommerce brands that want to manage their own blockchains; and Bitcoin, the cryptocurrency that led to the development of blockchain technology and allows customers to make purchases in sites and apps that accept Bitcoin as payment.

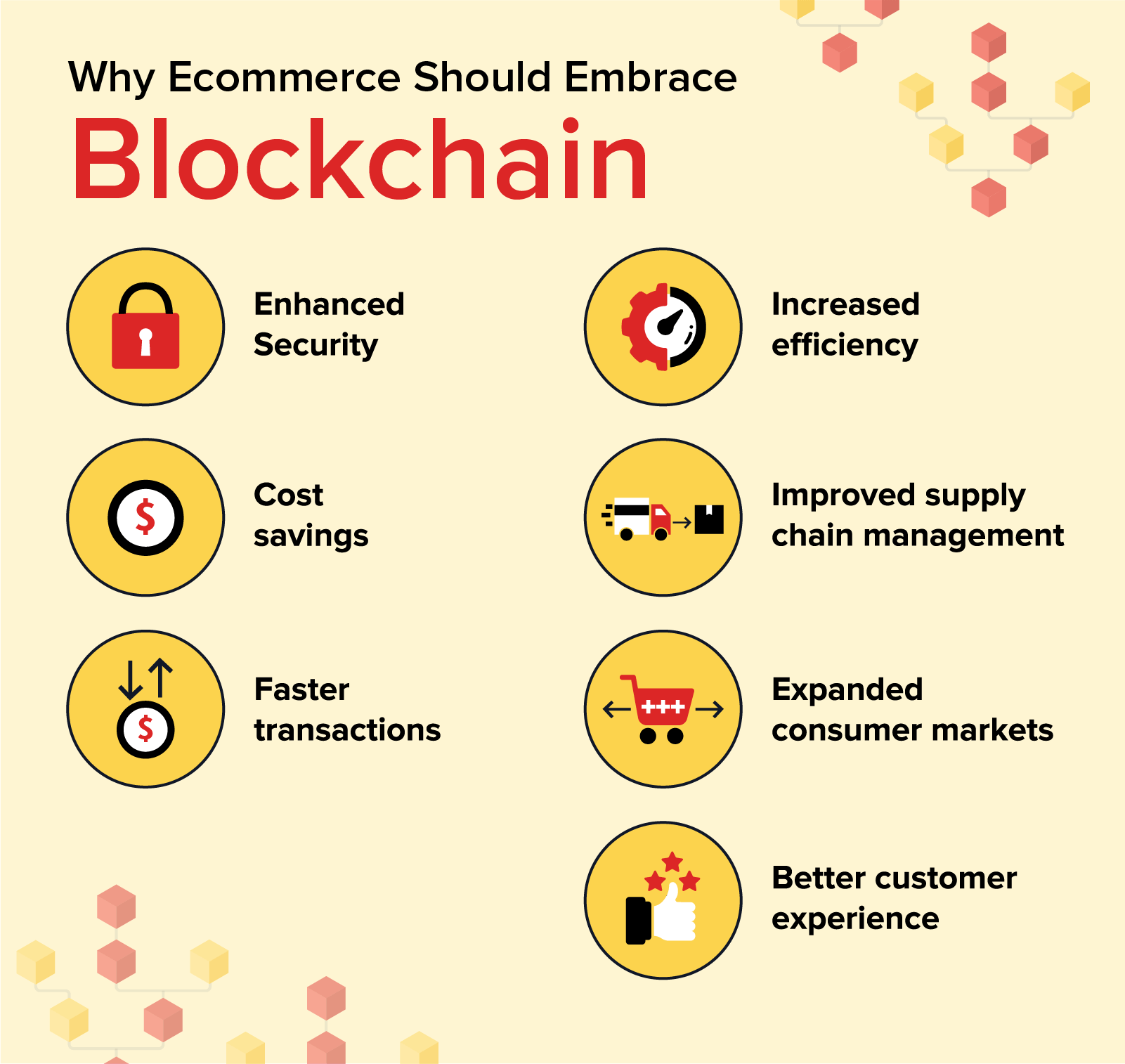

Benefits of Blockchain in Ecommerce

Because it makes online financial transactions more secure, blockchain is a win-win for both brands and buyers. But it also provides a lot of other benefits, including cutting costs, improving business processes, making transactions faster, and improving the overall customer experience.

- Enhanced security. Data breaches and fraudulent transactions are major concerns for ecommerce retailers. According to PriceWaterhouse Coopers annual Global Economic Crime and Fraud Survey 2020, 47% of companies experienced fraud in the past 24 months with a total of $42 billion lost.*

Blockchain technology allows for trusted identities verified by multiple trusted parties, and offers the highest level of security for customer databases and CRM systems. - Cost savings. One big advantage of blockchain technology is that it allows retailers to combine services like payment processing, inventory management, product descriptions, etc. so that they spend less on buying and maintaining separate systems.

And because cryptocurrencies like Bitcoin can be sent instantly peer-to-peer, there’s no need to go through banking systems. This cuts down on fees charged by banks for issuing or acquiring funds, or fees charged by credit card companies to process payments. - Easier, faster transactions. Because blockchain transactions are basically instantaneous and do not go through traditional banks, there are no delays for payment processing or pending transactions. Purchases can be made instantly, which means faster order fulfillment for customers.

- Improved business processes. Blockchains can store more than just transactional data. They can store smart contracts (also known as smart properties and chaincode), which can automate tasks based on preset rules and if-then statements, like automatic payments or inventory management.

For example, you buy a Rolex online and pay a deposit via a blockchain-based cryptocurrency. You get a receipt held in a virtual contract. The retailer sends you the watch by a specified delivery date, and if it doesn’t arrive on time, the blockchain releases a refund of your deposit. If you do receive the watch, the blockchain releases your full payment to the retailer.

Blockchain can also store digital records like customer receipts and warranty information, making it easier to validate ownership and warranty validation, not to mention cut down on paper records. - Reducing cost and complexity of supply chain management. Blockchain in ecommerce supply chain means brands can cut the paper and manual work associated with shipping. Bills of lading for cargo can be placed on the blockchain at each stage of the supply chain, cutting down on administrative time/costs and making it easier to track shipments or verify product information and pallet weight.

And for products with expiration dates or certificates of authenticity, blockchain can ensure the validity and quality of inventory and reassure customers they’re getting what they paid for. - Greater access for global consumers. For customers living in developing countries, access to a reliable banking system is not a given. Blockchain and cryptocurrencies allow them to bypass the banking middle man, giving them access to a wider variety of ecommerce retailers. And it allows forward-thinking brands to tap into new and emerging markets.

- More convenient rewards and referrals programs. Blockchain allows brands to easily issue rewards points that are redeemable across a variety of sites and partner brands. Companies can even pay content creators or influencers in digital tokens, which can then be converted into their preferred currency.

The Opportunities of Blockchain for Ecommerce Apps

While the technology may be relatively new, there’s one big reason why blockchain ecommerce platforms are gaining traction: they benefit both merchants and consumers.

Industry experts agree that while the potential for blockchain technology is tremendous, it’s still in its earliest stages of adoption. Blockchain will grow to be integral to the new financial and ecommerce ecosystem.

Shivkumar M

Head Product Launches, Adoption, & Evangelism.Expert in cross channel marketing strategies & platforms.

Free Customer Engagement Guides

Join our newsletter for actionable tips and proven strategies to grow your business and engage your customers.